Whether you plan to leave wealth to your heirs or simply want to help them prepare for their own savings and wealth growth/preservation strategies, legacy planning and working with future generations, specifically millennials, is crucial in today’s financial world. As millennials have quickly taken over as the largest percentage of the work force, comprising about 45% of the US labor market, they still have many lessons to learn.

That’s where Gen Xers and Baby Boomers play a major role – millennials have witnessed a very turbulent time in the markets, and therefore are unsure of the equity sector, fearful of experiencing what their parents went through in 2000-2001 and 2008-2009. This fear has kept them from approaching financial professionals, instigating them to keep the majority of their net worth in cash. This resistance produces a large problem: by investing in cash, millennials are not only falling behind over time as inflation will inevitably tick back up, but they are digging themselves into a hole that will require significantly more saving down the road.

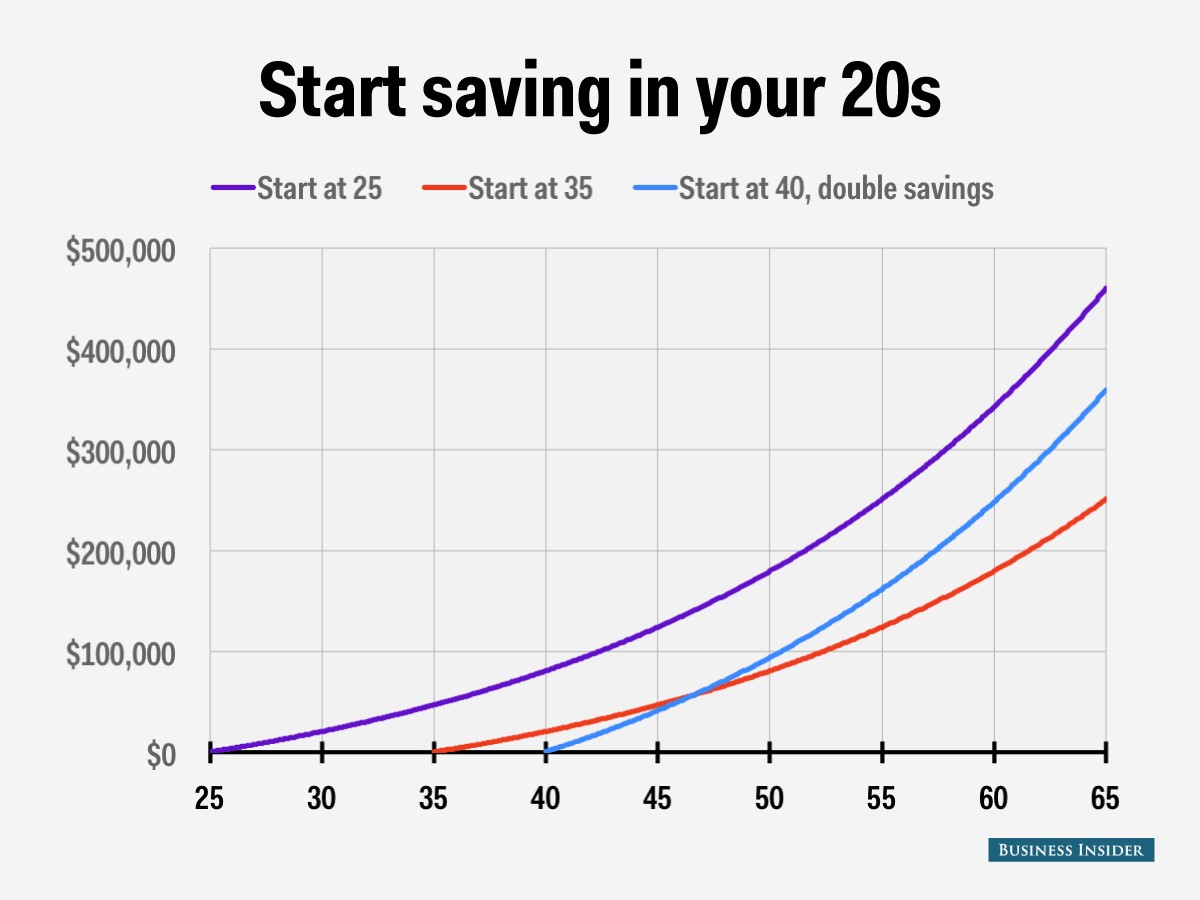

Compounding and the time value of money are key themes in financial planning. Simply put, the more you save earlier, the less you have to save later. However, if you wait to save, the opposite occurs, and you will be forced to sock more money aside.

In the below chart, three hypothetical investors develop a savings strategy: the first begins investing $300/month starting at the age of 25; the second investor waits 10 years and also invests $300/month; the third waits to invest at 40 but invests $600/month, double the other investors. As you can clearly see, by investing earlier, you require a smaller savings rate but will earn more over time. To see how much money each investor put in over time, as well as other specifics, please read the entire Business Insider article by clicking here.

At TBH Franklin, Travis, Ann, and I work closely with grandparents and parents to begin including future generations in meetings and discussions to get them accustomed to what a relationship with a financial advisor and planner looks like. We’ve found that by doing such, they become less fearful of the markets and much more open to creating a savings strategy of their own. However, that conversation usually starts at home with family members. Therefore, we encourage you as Gen Xers and Baby Boomers to speak with the younger members of your family today to explain the importance of a good financial plan, and we urge you as millennials that are reading this blog to speak with your elders, mentors, and someone within the industry – it’s never too early to form a comprehensive plan to put you in a position to save for your future.

There are also many other estate/legacy planning techniques, such as owning real estate or other hard assets that will allow for a step up in basis upon death, utilizing trusts to avoid taxes and pass wealth, or purchasing life insurance if your specific financial plan should require it. For these more in depth discussions, we would love to open up a dialogue, as we have a great network of estate attorneys, CPAs, and Travis’ in depth expertise within this arena as a Certified Trust and Financial Advisor (CTFA) that allow TBH to effectively coordinate with other professionals to develop a detailed estate plan for you and your family.

If you have any questions or comments, please call us at 615-465-6397 or click here to get in touch.