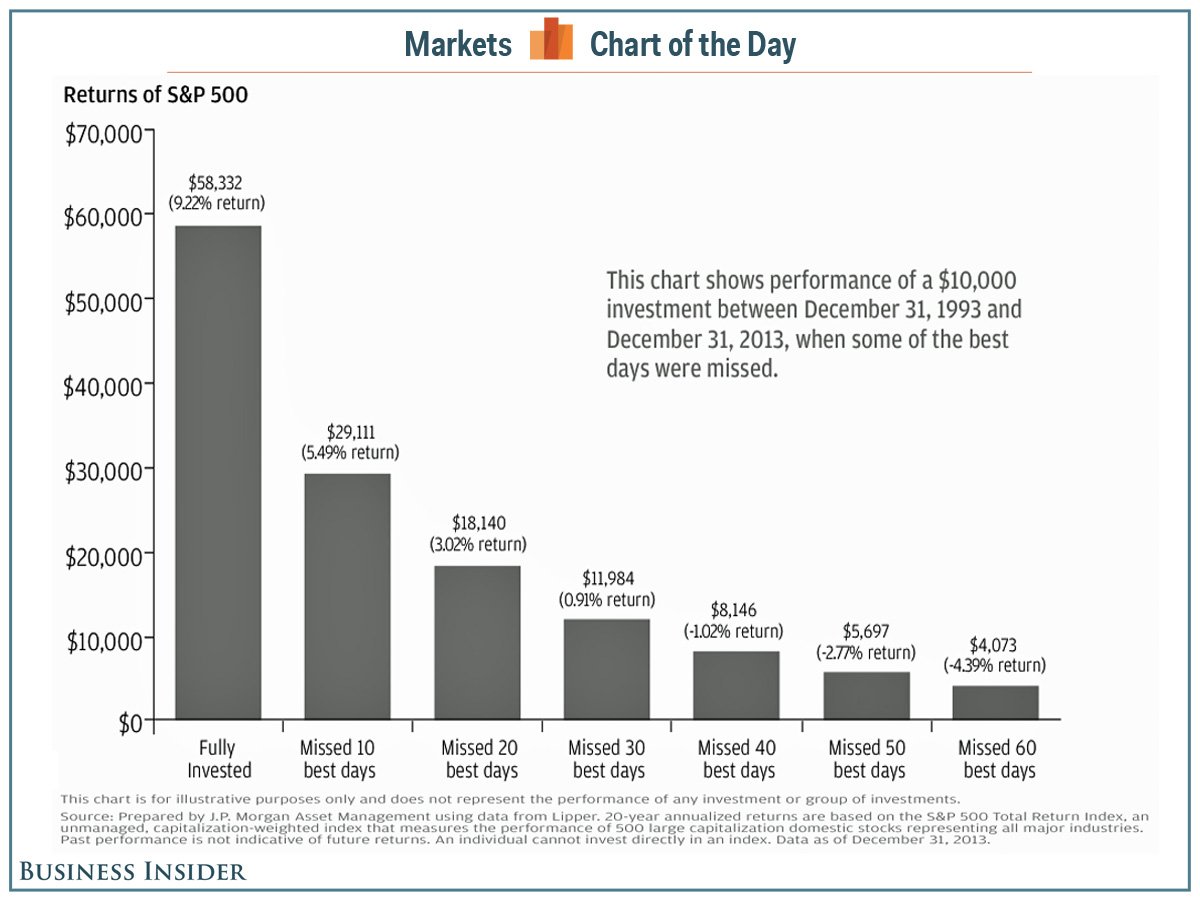

With May already here, if you haven’t already heard the May Cry, you’ll inevitably read the paper, a magazine, or watch CNBC or Bloomberg, and you’ll see that someone is telling you to “Sell in May and go away,” claiming that we’ve already seen decent returns (the S&P 500 is currently up about 2.25% year-to-date as of 4/23/15) and saying, “Why risk a pull-back, especially given the performance for the past 6 years?” Such a strategy might appeal to short-term investors or day traders; however, this approach can be detrimental to both long-term and short-term returns. As you can see in the below chart, trying to time the market from 1993-2013 may have allowed you to miss some of the bad days, but if you missed even the 10 best days, it cut your annual returns nearly in half. If you missed more than 10 days, your returns only continued to dwindle, eventually resulting in annual losses.

As you might recall, a lot happened within that 20-year timeframe – the Internet Bubble in 2000 and the Mortgage and Credit Crisis in 2007-2008 to name a couple. So, you might be asking how one should prepare to withstand recessions, such as the ones mentioned previously, going into the remainder of 2015 and beyond.

First, stay invested. Work with your financial professional to reinforce your risk tolerance. Investors tend to take on risk when things are good and shy away from risk when things are bad, a somewhat backwards way of thinking. Leading up to 2008, many folks took on additional risk through equity exposure, hoping to gain just enough in excess returns to buy that new car, retire a little earlier, or take an extra vacation. However, they took on risk when times were good, saw a big drop in 2008, got scared, and sold out of the market. Had they considered downside protection initially, they might have fared better on the way down, stayed invested, and taken advantage of the drop to gain excess returns going forward. Right now, we’re in one of those good periods so step back and really think about how much you could stand to lose without panicking. Talk with your family, come up with that number, and then reach out to your advisor so that any adjustments can be made if needed.

Second, diversify your assets. Riskier investors tend to like concentrations, which can create great returns but also great risk. If you are comfortable taking that risk, then continue on; however, for the rest, consider diversifying, creating an allocation among many holdings, sectors, asset classes, countries, etc. Some investments might go up, while others go down, but over the long haul, you can accomplish returns commensurate with your risk tolerance, while hopefully reducing volatility, i.e. those big swings up and down.

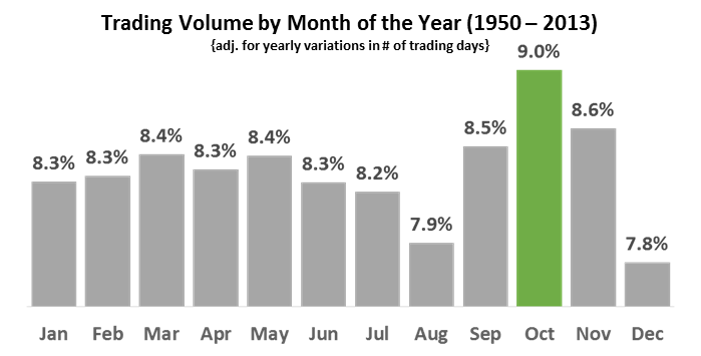

Third, consider current market conditions. We just read the word “Volatility,” which has been at bay for quite a while now but historically tends to rise in the summer months. You may have heard the phrase “Summer Doldrums,” which explains the phenomenon of reduced volume during the summer months. As you can see below, the chart shows that from June to August, you can see a sharp downtrend in average trading volume. With that reduced volume comes increased volatility – with fewer trades, the trades that are placed will have a higher impact on either the positive or negative price movement.

So, what is a good strategy to curb the increased volatility of the summer months? Reduce the ‘Beta’ of your portfolio. Beta is a measurement of correlation to the general market. If a stock has a beta of 1, it moves in sync with the market. Below 1, and it moves less than the market. Above 1, more than the market. Therefore, when entering periods of historically higher volatility, when considering risk management, we like to reduce beta in an attempt to minimize market swings, especially sharp moves downward.

In conclusion, really think about your financial goals and tolerance for both upside and downside returns, work with your advisor (or reach out to us at TBH Franklin if you are not currently working with someone) to determine your risk tolerance and investment needs, and create a diversified allocation to reduce volatility, while maximizing the opportunity for long-term returns.